Jun 3, 2026

I’m in an Investing Cult. Are You?

Remember Adam Aaron? He’s the CEO of meme stock AMC Entertainment. In early June of 2021, Adam was doing a video podcast interview when he fumbled his laptop camera, revealing that he wasn’t wearing pants.

Within about two weeks, AMC stock was at an all-time high.

While the high didn’t last long, AMC arguably got another two years of a higher-than-it-economically-deserves valuation.

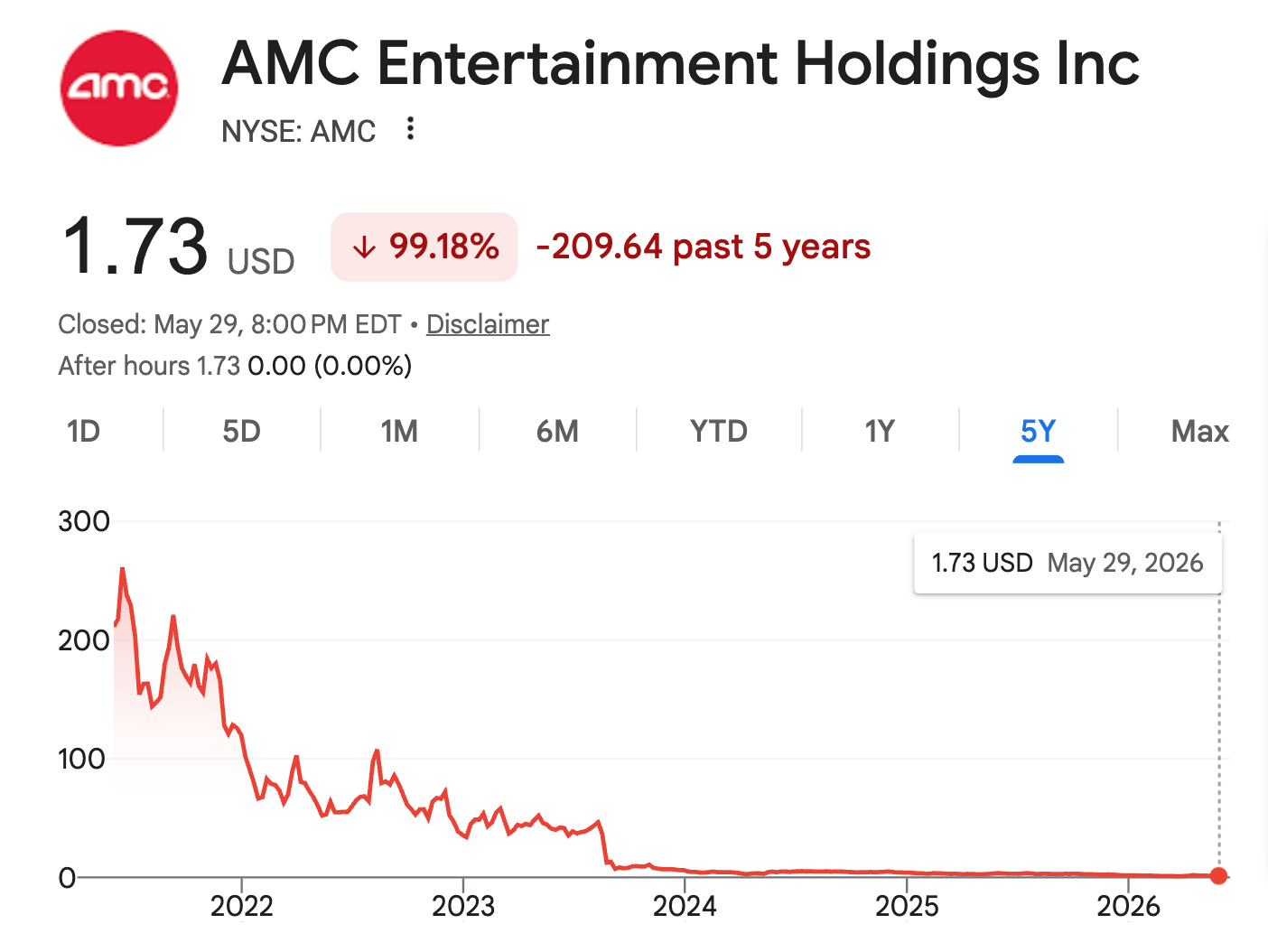

AMC’s market cap is now $1 billion, despite AMC having raised $4.7 billion in secondary offerings since the meme stock era started.

Rationality prevailed – but things got pretty irrational for a while, and took a few years to correct. My prediction? Markets will have more irrationality going forward.

It’s easy for rational investors like you and me to point fingers at the AMC “Apes” – AMC’s loyal tribe of shareholders who were really only loyal as long as they thought they could make quick money.

Or to point fingers at the capital-incinerating NFTs, which doubled as a fascinating social science experiment. Or anything crypto.

We point fingers because these things are bad for rational markets, and rational markets are good for both individual investors and the economy writ large. When investors are investing for non-economic reasons – tribalism, Greater Fool reasons, financial influencers on social media – economic-based price discovery gets muddied, making markets less attractive to the rational money that has traditionally been their backbone.

Smart money avoids the casino.

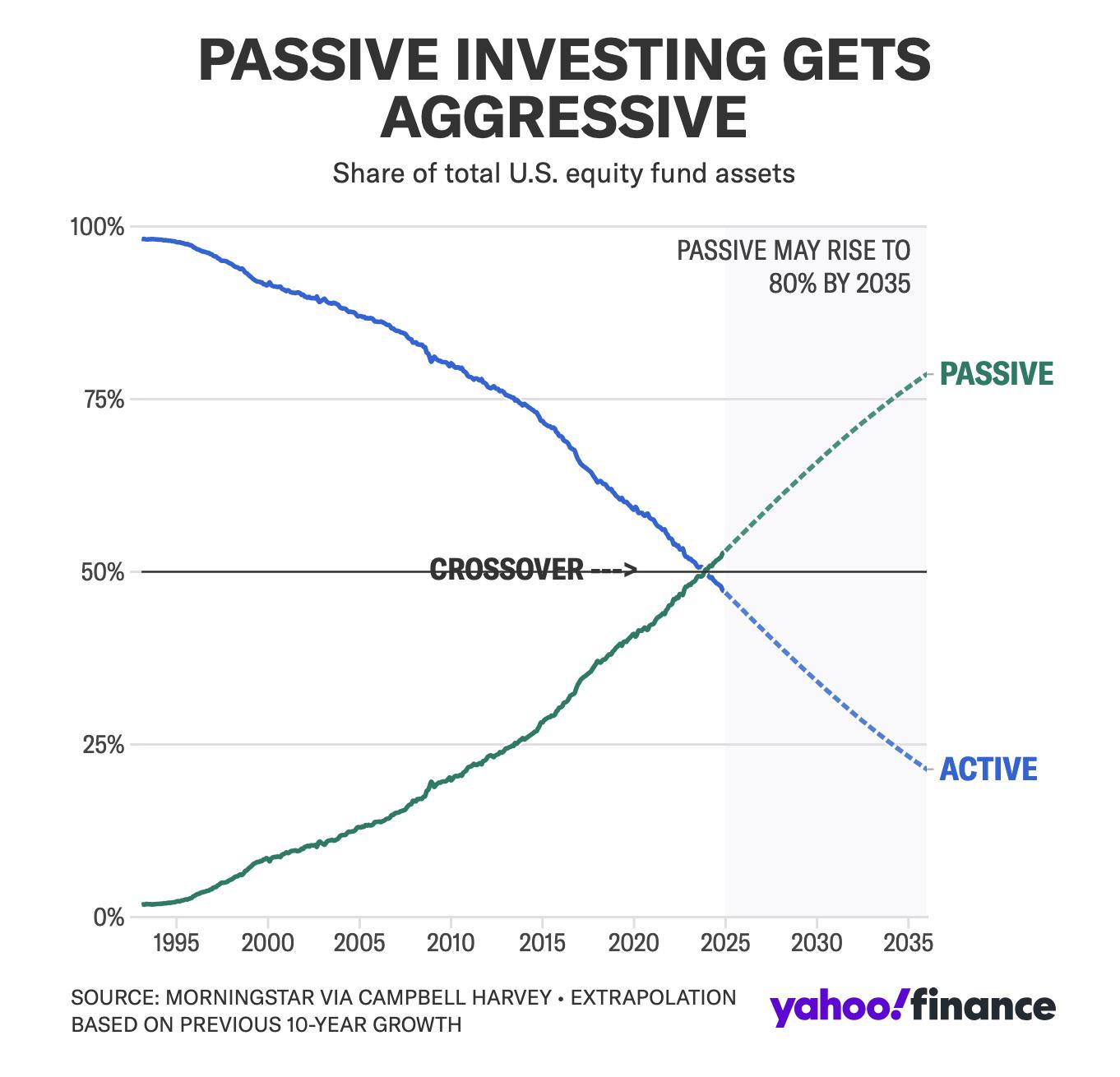

I could point a finger at passive investing (something I participate in and have endorsed many times), too: It’s great for individuals because it’s cheap, but if too many people do it, it’s not ideal for society because it mindlessly invests based (usually) on a binary factor: Whether or not a stock is in an index.

And unless you’re paying a little more to buy an equal weight fund, your passive money is momentum money: You’re making a big bet on Nvidia and AI if you own a regular, cap-weighted S&P 500 fund, and you’re probably less diversified than you’d expect to be for owning 500 stocks.

Passive investing deprives an economy of discrimination: Informed investors giving, after careful research and thought, capital to good, deserving companies and keeping it away from bad ones.

But passive investing is defensible because its alternative – active investing, which is by definition about this benevolent corporate discrimination – statistically performs terribly: Dow Jones S&P found that over any rolling 20-year period, 94% of US large-cap fund managers can’t beat the S&P 500. A 2002 paper by Joshua Coval, David Hirshleifer, and Tyler Shumway found that just 10% of individual investors beat the market in a given year.

Arrogantly, I’ll say that my former stock research service outperformed the S&P 500 for the 10 years I ran it, but statistically, I’m an outlier: Many (some would say most) managers are fee-charing clowns.

What about those rare investors like Warren Buffett or Markel’s Tom Gayner who have long records of beating the market?

Well, Berkshire Hathaway’s shares haven’t beaten the market for the past 18 years. Markel’s have underperformed for about the past 23 years. (In both cases I was quickly eyeballing the charts on Yahoo! Finance; more precise numbers can be had).

But Berkshire has delivered nearly 4,000,000% returns since 1965, when Buffett began using it as his holding company, and Markel has delivered more than 20,000% since its 1986 IPO. Even with a few decades of sub-market performance, both companies have earned returns great enough to create cult followings.

An irrational love of rationality

As a member and annual meeting attendee of both Berkshire and Markel “tribes”/cults, I have to say that there’s a coming-full-circle element wherein many tribespeople are such superfans that they’re judgement-impaired. Not to the extent of no-pants buying, but judgment-impaired nevertheless.

I’ll explain more next week.