Dec 23, 2025

3 Stocks for 2026

Dec 23, 2025

Our CEO, editor in chief, and investing Swiss Army knife - covering income, macro, and a bit of everything else with a unique flair for storytelling. James is the former Director of Research & Analysis for The Motley Fool, CEO of Stansberry China, and Chief Investment Officer of BBAE. The last time he ran a premium recommendation service, it beat the market 10 out of 10 years in a row across the most turbulent decade of the past century.

Read moreFrom investing ideas, to interviews with luminaries, to contentious roundtables, to conventional wisdom at unconventional times, Curia Financial brings you fresh, above-the-fray thinking.

Jun 25, 2026

Are you a rational investor? Or are you trying to approximate a rational investor? There's a difference.

Read more

Jun 13, 2026

Berkshire Hathaway built its returns on Buffett's rational investing, but its fan frenzy is far less rational.

Read more

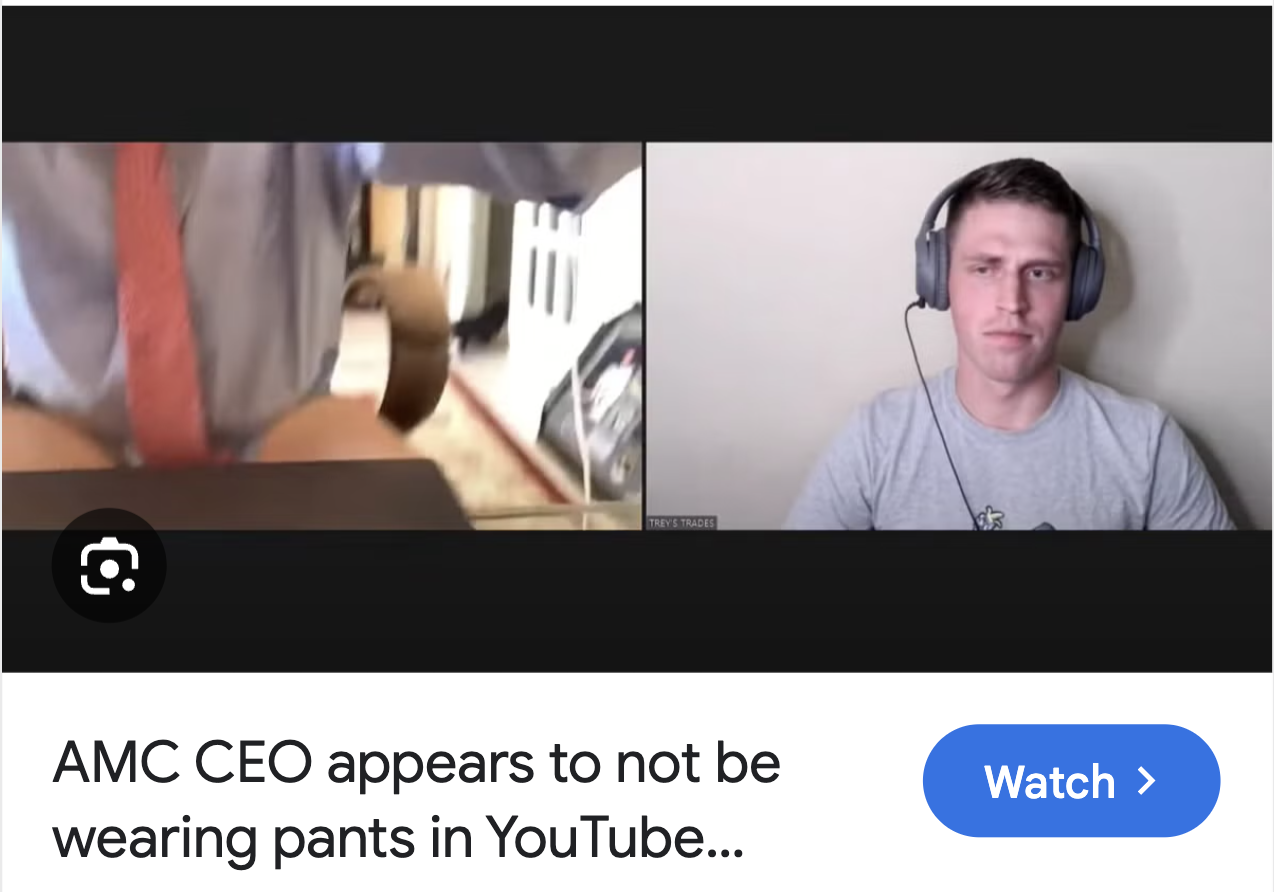

Jun 3, 2026

Remember Adam Aaron? He’s the CEO of meme stock AMC Entertainment. In early June of 2021, Adam was doing a video podcast interview when he fumbled his laptop camera,

Read more